![]()

Content

Reminder on the regulations

The " Choice of brand " feature allows merchants to comply with European regulation 215/751 of 29 April 2015 relating to interchange fees for payment transactions linked to a card, generally called "MiFID regulation" ( Merchant Interchange Fees ).

One of the objectives of this regulation is to remove the monopoly of local schemes by letting the consumer choose the brand used during payment.

Merchants have been required to comply with this regulation since June 9, 2016 .

Article relating to the regulations on the FEVAD website.

Trademark principles

Cards issued by French banks are largely attached to the French Cartes Bancaires (CB) network but also to an international network (Electron, Maestro, Mastercard, Visa, etc.). This is what allows the cardholder to use his card abroad. There are other local networks that issue co-badged cards. In Belgium, banks issue cards that belong to both the Bancontact network and also Maestro or Visa.

![]() Note : there are non-co-badged cards for which the regulations do not apply.

Note : there are non-co-badged cards for which the regulations do not apply.

As soon as a business accepts cards from different networks, it must allow consumers to select the brand they prefer.

If, for example, the merchant accepts CB, Mastercard and Visa cards, then the co-badged CB / Visa and CB / Mastercard cards are concerned, and the merchant cannot impose his choice. On the other hand, he can select his preferred network, which will be used if the consumer does not wish to change.

![]() Note : the network through which transactions pass can influence the amount of commissions applied by the acquirer. We invite you to contact your purchaser for more information.

Note : the network through which transactions pass can influence the amount of commissions applied by the acquirer. We invite you to contact your purchaser for more information.

Implementation

At the level of each Monext Online contract, the merchant can configure:

- The activation of branding : This option must be enabled to comply with MiFID regulations;

- The choice of default network for each type of card (debit, credit, business). This makes it possible to choose on which network the transaction will pass when the consumer does not make an explicit choice.

If the option is enabled, the consumer's choice always takes precedence over the merchant's default.

Regarding the Wallet , the network used by the 1 st transaction determines that used for the following transactions.

When activated on a contract, the "brand choice" functionality applies to transactions initiated in WebPayment ( Web mode, payment page and / or registration of a card in the Wallet ).

The manual entry of transaction in the backoffice allows the choice of the brand.

For the other modes, the collection of the choice from the customer is the responsibility of the merchant :

- DirectPayment : payment or payment by wallet, creation / modification of wallet;

- Batch Interface : authorization request function.

Configuration

Web mode

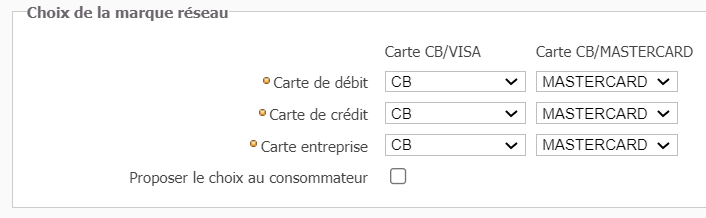

Choice of default network

In the configuration screen of a payment method in the backoffice, the merchant defines brand to be used by default according to type of card.

Consumer choice

In this same screen, the merchant must activate the functionality to leave the choice to consumer on payment pages.

![]()

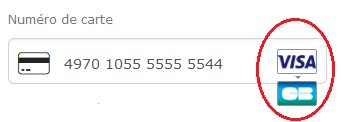

Brand choice on payment pages

When the consumer enters card number, the payment form will automatically offer the choice as soon as the card number is recognized as being co-badged.

The card logo is then transformed into a drop-down list, and the consumer can come and modify the default network.

![]() Note : If the merchant overloads the logos and / or user experience of payment widget, they must ensure that this does not alter the functionality.

Note : If the merchant overloads the logos and / or user experience of payment widget, they must ensure that this does not alter the functionality.

The payment receipt

The selected network is displayed on the ticket.

In DirectPayment mode

In the DirectPayment API mode, the merchant displays the payment form and collects the information from the consumer. It must offer a way to allow the consumer to select the brand (CB, Visa, Mastercard).

The Monext Online APIs can be used to pass information relating to the choice in order to comply with the banking protocol point of view with the acquirers.

To do this, the choice made by the consumer must be transmitted by filling in the cardBrand field of the Payment and Wallet objects with one of the following values:

- CB = 0

- VISA = 1

- MASTECARD = 4

- MASTER = 5

- BANCONTACT = 8

API webservices

Web service Monext Online | Comments |

Allow the merchant to transmit the brand to use ( payment.cardBrand field ) It is only taken into account if the payment method allows the brand choice. If the payment.cardBrand information is not present, then Monext Online uses the default brand configured in the contract. | |

Monext Online returns to the field:

| |

Monext Online returns the network to use in the network fields of extendedCardType and cardBrand of wallet. | |

Monext Online allows the merchant to transmit the brand to be used ( payment.cardBrand field ). It is only taken into account if the payment method allows the brand choice. If the payment .cardBrand information is not present, then Monext Online uses the default brand configured in the contract. | |

Monext Online allows the transmission of the brand in the cardBrand wallet field It is only taken into account if the payment methode allows the brand choice. If the Wallet.cardBrand information is not present, then Monext Online uses the default brand configured in the contract. The response message is not changed. | |

Same as createWallet. | |

Monext Online returns the network to be used in the fields extendedCardType .network and wallet.cardbrand | |

Monext Online returns the network to be used in the cardslist .cards and extendedCardType .network field | |

Monext Online returns to the field:

|

The screen for creating / modifying a wallet obtained after calling manageWebWallet supports the brand choice.

For recurring payments ( REC ), n times ( NX ) or wallet by web service, Monext Online sends the authorization request with the brand choice made during the 1st transaction.

Test card

The 4974132154654656 card allows a CB / Visa choice by the buyer on the payment interface in an approval environment.